44 / 84

44 / 84

subscription-based (SaaS) business ap-

plications, we have and will continue to

see a proliferation of new players and

new types of application categories,

says Forresters. For example, in the

e-commerce application category alone,

Forrester cataloged 45 subcategories

and nearly 500 vendors. All the while,

many non-incumbent providers have

been able to gain a significant foothold.

“The leading SaaS pure-play ven-

dors by revenue size continue to grow

at rates exceeding 20 percent,” finds

Forrester. Salesforce (23 percent),

NetSuite (35 percent) and Ultimate

Software (23 percent) all have enjoyed

sustained and consistent growth over

multiple years, says Forrester. Work-

day’s growth rates, though slowing re-

cently, have been even higher.

Indeed, “Forrester’s analysis of the

evolution of the business applications

market over the past decade indicates

that the large, traditionally on-premises

vendors (IBM, Infor, Microsoft, Oracle,

SAP) are losing share to faster-growing,

cloud-native rivals,” said the research

firm. The five largest traditional ven-

dors, named above, will go from a col-

lective business process applications

share of 25 percent in 2010 to a share

of 21 percent in 2017.

SaaS pure-plays Salesforce, Work-

day and NetSuite, meanwhile, plus

SaaS converts Intuit and Adobe have

grown their collective share during the

same period from 4 percent to 11 per-

cent, says Forrester. “All other provid-

ers” – presumably the group telecom

channels would fall under – account for

just less than 70 percent of global busi-

ness application revenues.

Not that traditional providers have

fallen asleep at the switch. “Virtually

every traditionally on-premises software

vendor we have spoken with in 2015 is

seeing significant growth in subscription

revenues and flat to declining license rev-

enues,” said the Forrester study on the

business process application market.

In terms of the overall size of the

opportunity, Forrester’s global mar-

ket analysis indicates that the core

business process applications seg-

ment, supporting both customer and

efficiency-focused solutions, will grow

from $141 billion in 2015 to $156 bil-

lion in 2016 and $169 billion in 2017.

Among the primary categories that fall

under “business process applications”

are customer relationship management

(CRM), call center/contact center sys-

tems, human resource management

(HRM), product lifecycle management

(PLM), e-purchasing, and specific prod-

ucts within financial management such

as accounts receivables.

“The market is a dynamic one be-

cause clients are continually looking

for new packaged apps for increasingly

specialized business processes,” say

Forrester researchers.

U.S. sales dominate and set the

pace of the market, with 52 percent of

the $156 billion market for business

process applications in 2016 coming

from purchases in the U.S., Forrester

estimates. An additional 5 percent will

originate in Canada and Latin America.

CRM, commerce servers and human

resources management are the fastest-

growing categories of process apps, at

20 percent, 17 percent, and 16 percent,

respectively, reports Forrester.

SaaS business process applications

represent about one-third of the market

currently and will grow by 24 percent

in 2016, significantly faster than the

overall market, which has a 12 percent

growth rate. The U.S. share of the global

SaaS process application market is

even higher than the overall, rising to 64

percent, up from 61 percent in 2013.

Once again, SaaS subscriptions are

driving revenue growth for the business

applications landscape, as license reve-

nues decline and maintenance revenues

grow at a slower pace, says Forrester. In

2012, subscriptions represented $22

billion in revenues; in 2016, Forrester

projects that subscriptions will be $53

billion. Looking beyond 2017, Forrester

expects SaaS subscriptions will con-

tinue to grow rapidly through 2020, gen-

erating more than half of total software

revenues by 2020.

That’s partly because a quarter to

a third of enterprise buyers surveyed

by Forrester in the fourth quarter of

last year said they plan to replace

most or all of the 12 types of business

applications covered by the Forrester

study with SaaS within the next two

years. In addition, 19 percent to 23

percent have already replaced these

applications with SaaS.

“While SaaS adoption is growing

in all process application categories,

adoption rates vary widely across

categories,” according to Forrester

researchers.

In 2016, for instance, more than

half of all product revenues in CRM,

commerce servers and e-purchasing

will come from SaaS subscriptions. The

SaaS share is even higher in some sub-

categories in marketing automation in

CRM, as well as services procurement

and network services in e-purchasing,

where 80 percent to 90 percent of rev-

enues are from SaaS subscriptions.

All the while, human resources

software, risk management and pay-

ment, and supply chain management

(SCM) apps are tilting toward SaaS,

anies studied

Source: Forrester Research

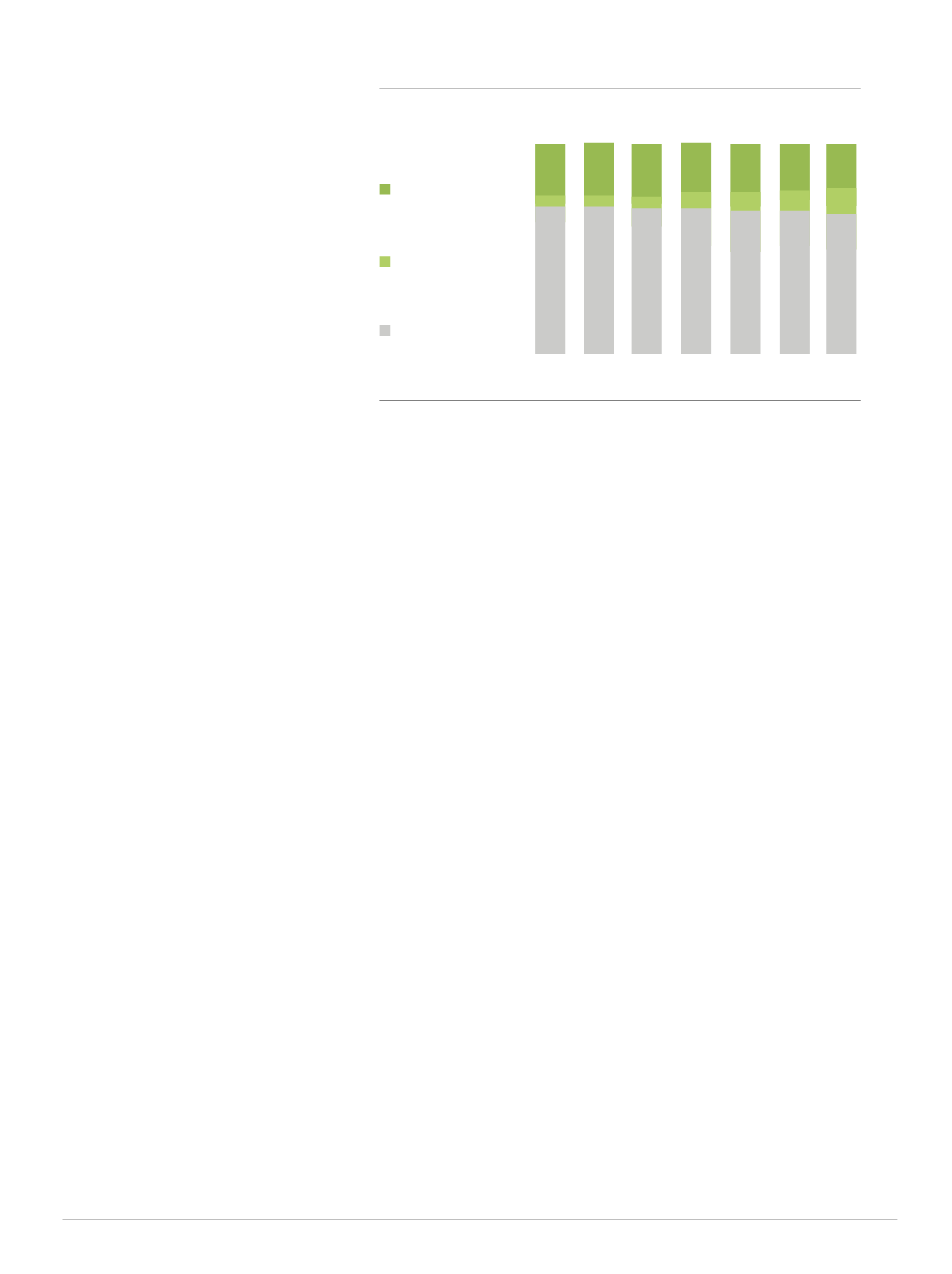

Global application revenues by type of vendor

(percentage of total market share)

ch

ers

2015 2016 2017 2018

earch

Mobile Search

$58,095,571

$60,525,947

$65,047,302

80,000,000 $75,000,000

Five leading traditional

process app vendors

(IBM, Infor, Microsoft,

Oracle, SAP)

Five leading SaaS

process app vendors

(Adobe, Intuit, NetSuite,

Salesforce, Workday)

All other vendors

26%

5%

69%

26%

6%

69%

25%

6%

68%

24%

8%

69%

24% 23% 22%

8% 9% 10%

68% 68% 67%

2011

100%

100%

80%

60%

40%

20%

0%

100% 100% 100% 100% 100% 100%

2012 2013 2014 2015* 2016* 2017*

Source: Forrester Research

Global business process pplications product rev nues

by type of r venue

Software-as-a-service (SaaS) subscription as

a percentage of total product revenues 2016

Maintenance revenues

Licenso revenues

Software-as-service

(Sa S) subscription revenues

2011 2012 2013 2014 2015* 2016* 2017*2018* 2019* 2020*

(percentage of total revenue)

Customer relationship management

Commerce servers

ePurchasing and business networks

Human resourc s management

Risk management and payment

Supply chain management

Governance, risk, and compliance

Financial management systems

Product life-cycle management

Call center/contact center systems

56%

55%

53%

41%

38%

30%

23%

22%

11%

10%

2020

44

CHANNEL

VISION

|

July - August 2016