The channel can play a pivotal role in rollout of IoT solutions

For the uninitiated, it’s easy to think of an enterprise Internet of Things deployment as little more than “dollars per boxes” and some low-bandwidth circuits. It’d be more accurate to think of IoT as “touching everything.”

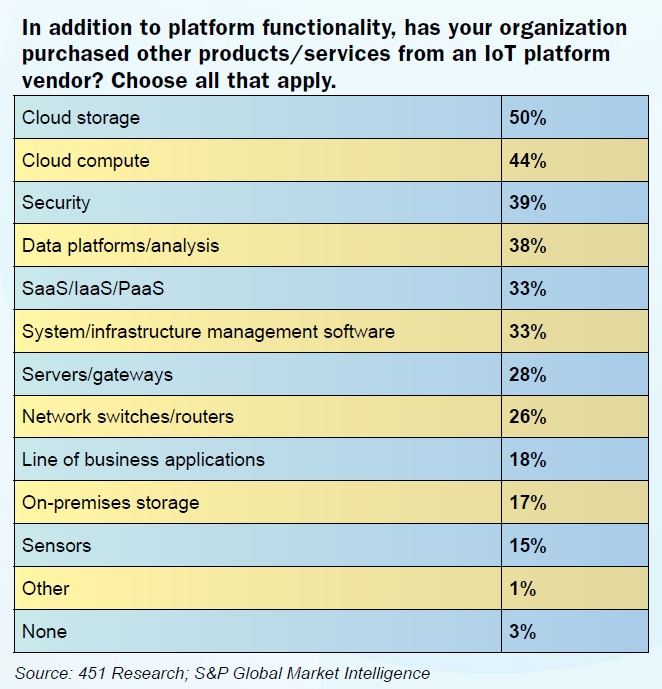

As IoT projects and budgets continue to expand, deployments are becoming less about clusters of siloed IoT devices and more about fully interconnected and autonomous IoT environments. In turn, it’s not uncommon for an IoT implementation to involve a number of other systems and solutions such as security, storage, data analysis, compute, backhaul, on-going monitoring, managed connectivity, private wireless and vertical specific capabilities, among other functions and features.

In many cases, all or most of those services are critical to reaching intended outcomes. In other words, IoT is certainly more about selling and deploying a “platform” than a “service.”

If that sounds complex, it’s because it is. And early adopting enterprises have had to work hard to piece together IoT projects – which tend to encompass many technologies and integration points, while unleashing an onslaught of data – and move those projects out of trial and into enterprise-wide production. Not that this has persuaded adoption or soured adopters. Surveys suggest IoT budgets are growing healthily, and the vast majority of early adopters are satisfied with initial results. As much as 93 percent of respondents surveyed by 451 Research described their IoT initiatives as “successful,” including 38 percent dubbing them “very successful.”

For the next stage of adoption to occur, however, things will need to get much easier for customers. And as the business IoT platform providers pull the ecosystem together, it appears there’s a clear role for channel partners and providers of network and communication services.

Make no mistake, despite the emerging long tail of IoT platform and solutions vendors, the major hyperscalers and larger, well-known IT vendors have pulled ahead in terms of offering “IoT platforms” that are integrated with related infrastructure and technologies (emphasizing the importance of cloud compute, storage and data analytics to IoT outcomes). And these types of platforms sit at the center of most IoT enterprise deployments.

Among enterprises surveyed for 451, a division of S&P Global Market Intelligence, the most widely deployed IoT platforms come from Microsoft (used by 38 percent of respondents), followed by AWS (30 percent). AT&T comes in third at 28 percent, the first time the company ranked that highly, the study noted, with IBM (18 percent) and Google (17 percent) rounding out the top five. Microsoft was also the highest ranked “primary” platform vendor at 24 percent, “reflecting the ongoing trend of industry platforms often running on top of cloud IoT infrastructure,” said the research group.

Most initiatives also involve a systems integrator or consultant type that holds some expertise in the enterprise IoT platform of choice, said the research firm. And in addition to those key partners, enterprises work with an average of nine vendors in their IoT projects, providing elements including connectivity, security, premises gear, analytics and integration, among others. When choosing those vendors, enterprises value above all else the ability to consult on and deliver “best of breed” technologies, suggest the 451 surveys, more than IoT-specific expertise, cost, ability to deliver outcomes and vertical expertise.

“IoT platform/infrastructure vendors often sit at the center of such projects, but other providers are also critical,” wrote Rick Karpinski, principal analyst at S&P Marketing Intelligence. IT service providers and consultants help from deployment through data analysis, while vertical application vendors, especially in the industrial sector, play a key role as well, he continued. “Coordination of those vendor relationships and a pilot-to-production, edge-to-cloud view of how IoT technologies fit into enterprise-wide architecture choices are essential.”

Enterprises are pretty evenly split between a build, buy or partner approach to creating their IoT ecosystems. The largest group, at 38 percent, choose to “build,” assembling individual pieces on their own, while 31 percent buy pre-integrated platforms, applications and services, and 30 percent enlist partners such as cloud providers and systems integrators to do the heavy lifting. The three choices “are certainly not mutually exclusive,” said Karpinski, as many organizations likely leverage all three approaches.

More than half of respondents said they have used an opex or “as-a-service” mode of purchasing IoT infrastructure and applications, while a similar 51 percent claim to have opted for a capex approach to purchasing.

Also of note, 33 percent of respondents said they have opted for an “outcome-based” approach to at least part of their IoT initiatives, paying IoT providers based on the delivery of successful business outcomes.

Challenges & Opportunities

Among the many opportunities up and down the IoT value chain, a few areas stand out, both in terms of their compatibility with the existing specialties of the network and communications services channel as well as the primary challenges faced by IoT buyers. Namely, those include interoperability/integration, cybersecurity and managing connectivity.

While the IoT ecosystem is forming rapidly, as of now IoT platform providers tend to draw the demarcation line at where their services and devices end and an organization’s internal operations start. Buyers have had to fend for themselves or turn to the providers of their other internal systems to add-on and integrate in ways that deliver intended business outcomes.

“[T]he IoT industry hasn’t achieved a genuinely seamless experience in which devices pass into and out of physical environments and are identified, trusted and managed without a need for separate (and at times manual) authentication steps,” said analysts in McKinsey & Company’s IoT practice.

Much of the value of an IoT deployment, all the while, comes from the ability to provide that seamless experience, argued McKinsey analysts. Various devices must communicate through heterogenous operating systems, networks and platforms, often through cloud-based data storage and cloud-native programming, thereby empowering constant information exchange with a high level of autonomy.

“Imagine the ability to drop a new device into a network and have it immediately scanned, welcomed, and assigned a trust score,” said McKinsey.

We’re not there yet, leaving ample areas of opportunity for trusted providers that can help with effortless integration within and across tech stacks of devices; grease processes with sign-in efforts, self-managed devices and over-the-air patch updates; and simultaneously leverage multiple connectivity standards, platforms and back-end systems.

“The ability to develop seamless experiences will likely spur further adoption of the IoT, as it helps address critical factors such as confidentiality, connectivity performance, cybersecurity, installation, interoperability, privacy and technology performance,” said McKinsey’s IoT experts.

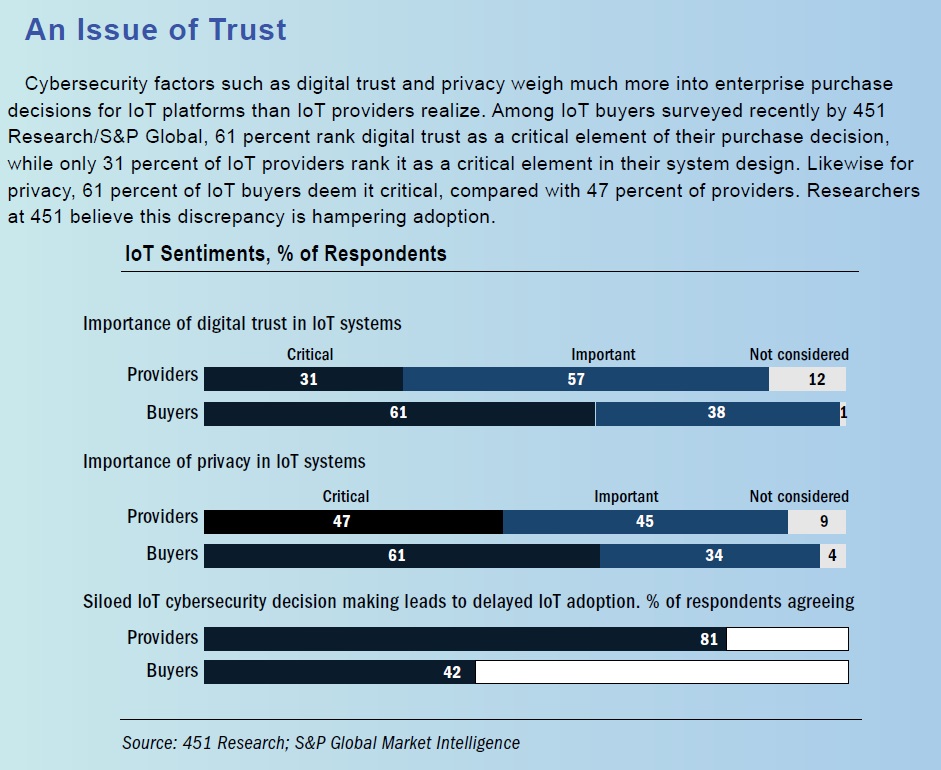

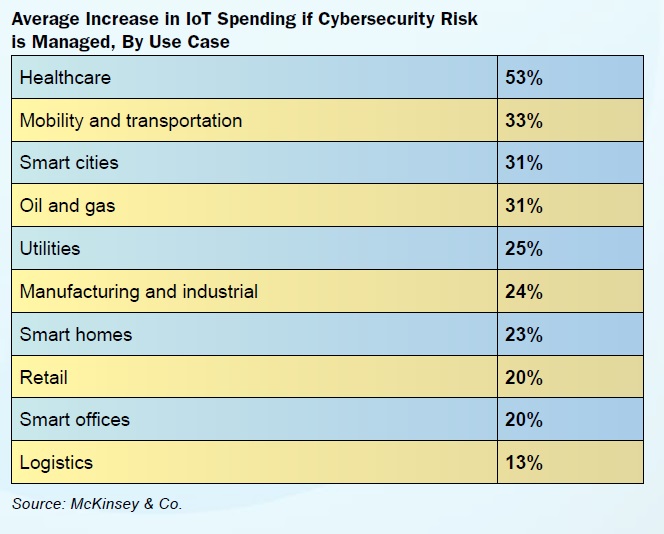

Among the areas of integration, cybersecurity stands alone as the biggest challenge for adopters and arguably one of the biggest early opportunities for the value chain. Survey respondents across all industries cite cybersecurity deficiencies as a major impediment to IoT adoption, showed McKinsey data. Roughly 30 percent of respondents name cybersecurity risk as their top concern. Of these respondents, 40 percent indicate that they would increase their IoT budget and deployment by 25 percent or more if cybersecurity concerns were resolved.

Compared to enterprise IT, solution design in the IoT space lags behind in terms of security assurance, testing and verification, said McKinsey. This despite the possibility that risk profiles of many IoT systems are elevated compared with that of enterprise IT, given IoT’s control over physical operations.

“Cybersecurity risk multiplies due to the interconnectedness of IT and operational technology within the IoT, especially in use cases that involve the transmission of critical data or the operation of critical business processes,” said the research firm. Incidentally, IoT application software and human-machine interfaces are the most vulnerable layers of the IoT stack, McKinsey found.

Up until now, achieving a trusted level of IoT cybersecurity has been difficult, IoT buyers tell McKinsey. There is little multilayered security embedded in today’s IoT solution designs, leading to vulnerabilities that require regular over-the-air updates and patches, which can be difficult to implement. Most providers in the space have tended to treat cybersecurity as a separate software category, providing bolt-on solutions rather than making security a core, integral part of the IoT design process.

In turn, IoT buyers are taking on an enormous responsibility of protecting the IoT value chain, argue McKinsey analysts. “They typically do so by partnering with cybersecurity vendors to provide add-on solutions. These tend to be enterprise-wide cybersecurity solutions rather than IoT-specific products, with additional security features bolted on later as needed.”

“Enterprises struggle to understand the security risks that IoT devices bring to their network and technology ecosystems,” agreed Gartner analysts. “Enterprise investment in IoT security is generally insufficient and reliant on provider security.”

Here again, the value chain ecosystem is rapidly forming. Approximately 80 percent of IoT providers surveyed by McKinsey are embedding security in some form into their IoT products, and roughly 70 percent of cybersecurity providers are making IoT-specific products. Further indicating early signs of convergence, approximately 60 percent of providers are partnering with security specialists to offer comprehensive IoT and cybersecurity solutions rather than building those capabilities in house. About half of providers, meanwhile, are building what McKinsey described as more “holistic solutions for both cybersecurity and the IoT.”

Even so, “it’s hard to create a one-size-fits-all solution for cybersecurity needs across different verticals and use cases,” McKinsey researchers continued. “Specialized companies will continue to play a role in IoT and cybersecurity operations because of their differing functionality, their heterogenous operating systems and the lack of standard interfaces and criteria across regions, industries and requirements.”

Getting Connected

Things haven’t been all that much easier when it comes to managing connectivity. IoT deployments tend to require a bundle of connection technologies (LTE, wired, satellite, low-power wide-area (LPWA) networks, etc.) in addition to a few emerging standards. Among providers of managed IoT connectivity, for example, connections reported in Gartner’s most recent Magic Quadrant report on the subject showed 101 percent year-over-year growth in 3GPP LPWAN, moving to 20.5 million from 10.2 million and representing almost 12 percent of the overall net growth of all vendors.

“Enterprises see 3GPP LPWA networks with LTE-M and NB-IoT as the right alternative to replace existing 2G/3G deployments in countries where these networks are being sunsetted,” said the report.

Gartner also has observed several vendors adding private and public LoRaWAN to their portfolios and showing moderate growth, as well as vendors starting to test and integrate LEO satellite capabilities, including 3GPP WAN to satellite as an option for areas with no cellular coverage.

The gradual rise of eSIMs replacing branded SIMs, in particular, provides an interesting opportunity for attackers, argue its proponents. Offering the flexibility to switch between networks, eSIMs effectively break “vendor lock-in,” while offering means to reduce some costs and integration headaches. And the major hyperscalers are among those attackers. Meanwhile, Apple’s iPhone 14 already has an eSIM with a satellite overlay, allowing emergency texts via satellite, point out executives at IoT connectivity provider Eseye.

If nothing else, the primary role that connectivity plays within IoT efforts seems to suggest healthy growth in the demand for managed IoT connectivity as well as private networks.

Despite any nascency that remains within the larger IoT market, it’s certainly not dampening the enthusiasm among IoT buyers and potential adopters. Several surveys suggest satisfaction and intent is high, and most experts predict healthy growth for the category.

Quite simply, it’s hard to envision a picture of the future that does not include a myriad of connected devices that collect mountains of data, control environments and processes based on that data and seamlessly communicate with personal devices. And when considering the complexities to pull this off, it’s not surprising that a team of integrators, trusted advisors and third-party providers will be enlisted to bring this future to fruition.

Indeed, “this won’t be a winner-takes-all market environment,” McKinsey IoT experts conclude. “To maximize the opportunity for the IoT to play an increased role in many aspects of people’s lives, numerous players will have to work together to reduce risk, and numerous players will be in a position to reap the rewards.”